If prime cards keep declining, credit repair affiliate CPA programs are a safe way to save intent and stabilize EPC. Pair them with secured cards and credit-builder loans/apps as step-up paths. Whatever you promote: confirm offer-level allowed traffic in writing, send users through a pre-lander (eligibility, fees/timelines, disclosures), and review enroll/approval reasons weekly.

Key takeaways

- Routing ≠ losing: shift declined card traffic into repair/secured/builder to protect EPC.

- Offer rules win: permissions (SEO/email/social, brand terms) are per offer, not per network.

- Pre-qualification first: eligibility bullets + cost/timeline clarity reduce complaints and churn.

- Mobile decides: mid-range Android UX, error states, input masks, and fast LCP matter most.

- One change/week: keep cohorts clean (GEO/device/source/angle) for 7–14 days, then iterate.

When cards under-approve — what to route and why

In credit repair affiliate CPA programs, it’s common to see users who don’t qualify for standard credit card offers. Instead of losing that intent, smart routing helps you guide each profile toward a better fit — improving user outcomes and long-term approvals.

Common denial reasons include thin credit files, recent delinquencies, high utilization, short history, or mismatched income. Map these to the right next steps:

- Derogatories or disputes → Credit repair (education + dispute workflows).

- Thin or low-score users who can place a deposit → Secured cards (collateral-backed).

- No or limited history → Credit-builder loans or apps (predictable payments that report).

[pic] Routing diagram (Card denial → Repair / Secured / Builder).

Routing keeps your funnel clean, preserves traffic value, and sets users up for future approvals once their profiles improve — turning early denials into future wins.

Recover denied card traffic — Start with repair/builder on Leadgid.

Routing alternatives — quick comparison

When denied card users hit your funnel, the next move decides whether you recover EPC or lose intent. The best credit repair affiliate CPA programs don’t just stop at “no” — they reroute users to better-fitting solutions like credit repair, secured cards, or credit-builder loans. Each path fits a different user type, approval profile, and compliance framework. Understanding who qualifies for which route helps affiliates maintain trust, improve approval ratios, and stay within lender policies. Use this table to choose the right option for your GEO and channel — and to balance payout stability with long-term conversion potential.

|

Path |

Who it fits |

Pros |

Cons |

Compliance watch-outs |

|

Credit repair |

Users with derogatories or disputeable items |

Clear problem→solution; education converts |

Longer time-to-value; variable enrollment |

No promises; fair-use claims; required disclosures |

|

Secured cards |

Thin/low score; deposit available |

Easier approvals; builds history |

Deposit friction; potential fees |

Issuer copy rules; brand terms |

|

Credit-builder loans/apps |

Thin/no file; prefer installment routine |

Simple UX; build history predictably |

Smaller payouts; app store frictions |

KYC language; in-app disclosures |

When you shortlist offers, consider the best programs for secured credit cards and relevant credit builder loan programs for your GEO and channel.

[pic] Pros/cons matrix visual (three columns, icons).

Compliance & allowed traffic (offer-level)

Before promoting credit repair affiliate CPA programs, it’s essential to understand exactly what traffic types are allowed. Different offers have different rules, and compliance always starts with written confirmation from your account manager.

- Permissions can vary by channel — SEO, email, or social — as well as by brand bidding and pre-lander requirements. A frequent question is which credit repair programs allow SEO traffic — some do, but they often require clear disclosures and compliant content standards. Always double-check these details before launch.

- Avoid any “guaranteed” or “instant approval” claims; instead, use accurate phrasing like “check eligibility” or “subject to provider approval.” Email campaigns must use permissioned lists, and social policies evolve regularly. Link to each platform’s official policy page instead of paraphrasing or relying on old notes.

Pre-lander patterns (repair/builder)

A strong pre-lander turns denied users into qualified leads. For credit repair affiliate CPA programs, keep pages clear, neutral, and fast. Start with a simple hero line — no promises, just an invitation to check fit. Show who the offer suits and who it doesn’t. Explain fees, deposits, and reporting timelines in plain language. Outline the 3-step process — check → enroll → provider review. Always link to terms, privacy, and consent details, adding “subject to provider approval.” Use “Check eligibility” as your CTA. Add support info, local hours, and test everything on mid-range Android devices.

Your pre-lander for credit repair offers (and adjacent secured/builder pages) should include:

- Hero (promise-free): “Check if this option fits your credit goals.”

- Eligibility & fit indicators: who typically benefits; who doesn’t.

- Costs & timelines: deposits/fees, how reporting works, expected duration (no promises).

- How it works (3 steps): check → enroll/apply → provider decision/reporting.

- Disclosures/T&Cs: links to provider terms, privacy/consent; subject to provider/issuer approval.

- CTA: “Check eligibility” (not “Get instant approval”).

- Support strip: contact, service hours, language notes.

Localization: currency symbols, local service hours, repayment/payday cadence, and device QA on mid-range Android.

[pic] Pre-lander wireframe (repair/builder modules).

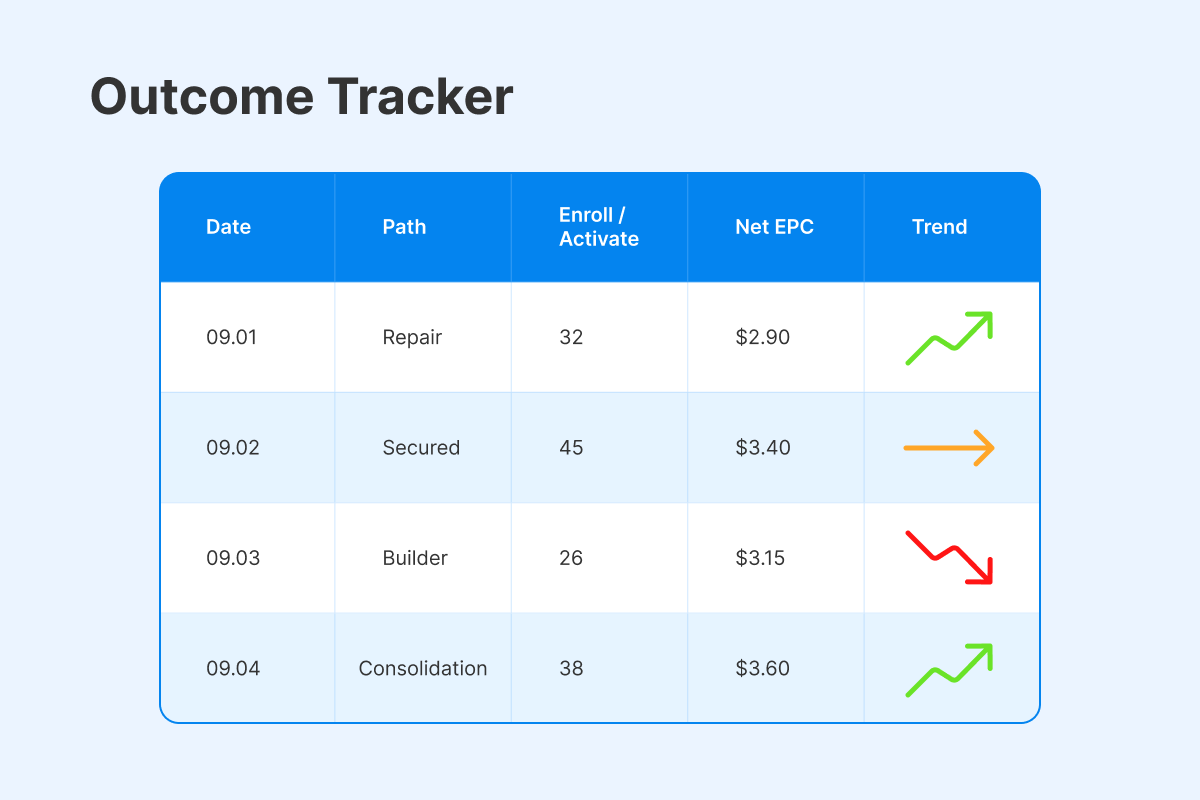

Benchmarks & Diagnostics (Repair/Builder)

When running credit repair affiliate CPA programs or credit-builder flows, it’s important to know what “good” looks like. Think of these as orientation ranges, not promises — results shift by GEO, traffic source, app design, and provider mix. Benchmarks help you spot whether an issue lies in copy, UX, or partner performance.

Typical performance patterns:

- Pre-lander CR improves with clarity — adding short eligibility and fee bullets can lift conversions by 10–20%.

- Enroll/Activation rate depends most on how clearly you explain fees or deposits and how smooth the mobile experience feels.

- EPC stability tracks closer to enroll and activation than to click counts — prioritize clarity and user flow before scaling traffic.

Quick diagnostics:

- Low enroll: clarify fees and deposits, reorder key sections, and add a micro-FAQ.

- Mobile drop-offs: compress assets, fix input masks and tap targets, add clearer error messages.

- Volatile EPC: check if cohorts are mixed; verify provider uptime and confirm no policy drift.

Need help picking a route? Talk to a manager.

Mini “How-to” — route in 5 steps

Routing is how credit repair affiliate CPA programs turn declined card traffic into active, monetizable cohorts. Instead of losing users after a denial, you can redirect them to the right next step — credit repair, secured cards, or builder loans — keeping intent alive and improving long-term EPC.

Here’s a quick framework to build a clean, compliant routing flow:

- Read denial patterns from your card cohort over the last 7–14 days. Identify top reasons for rejections (e.g., thin files, utilization, delinquencies).

- Shortlist repair, secured, or builder offers that fit your channel and GEO — and confirm each one allows your traffic type.

- Build and localize your pre-lander: show eligibility, fees, and timelines clearly; submit copy for approval.

- Launch one clean cohort (defined by GEO, device, source, and angle); enable postbacks and monitor EPC + Enroll/Activation.

- Run a weekly loop: log enroll and denial reasons → adjust eligibility or fee copy → test again and compare results.

Routing done right keeps your funnel compliant, efficient, and profitable — one steady cohort at a time.

Common mistakes (and quick fixes)

Even the best-performing credit repair affiliate CPA programs face one challenge — what to do with card traffic that gets denied. Instead of letting those clicks go cold, affiliates can recover value by rerouting users to credit repair, secured card, or credit-builder paths. Each option matches a different denial reason and keeps the user journey relevant, compliant, and profitable.

Routing is more than damage control — it’s a system for retaining intent, improving user experience, and lifting long-term EPC. By segmenting denials, maintaining compliant copy, and holding clean cohorts, affiliates can turn what looks like loss into a predictable revenue stream.

- Routing everyone to repair. Segment by reason; offer secured/builder where fit is better.

- Promise language. Replace with eligibility/education wording; add issuer/provider disclaimers.

- Ignoring deposit friction (secured). Explain deposit size, hold, and refund rules plainly.

- Mixing GEOs/sources. Keep cohorts clean; one lever per week.

- No evidence trail. Save policy screenshots, copy approvals, and test logs.

Routing isn’t a setback — it’s a strategy. When card approvals dip, smart routing keeps traffic profitable and users served. By matching denials to the right paths — repair, secured, or builder — you preserve intent and open new earning streams. Clear copy, compliant pre-landers, and clean cohorts make the difference between wasted clicks and steady EPC. With the right approach, routing becomes a growth lever, not a curse. Routing isn’t about chasing volume — it’s about precision. When you build with evidence, segment by reason, and keep the loop tight, denied traffic becomes a steady, compliant stream of approvals.

Weekly wins = clean cohorts. We’ll help map denial reasons to the right offers. Recover denied card traffic with repair/builder routes — Start on Leadgid.

FAQ

- When denials cite derogatories/disputes/late payments. Educate first, then invite to check eligibility; decisions are subject to provider approval.

- Users who can place a refundable deposit and need to rebuild history. Explain deposit and fees clearly to reduce drop-offs.

- They convert when timelines and payments are crystal clear, auto-pay is easy, and mobile forms are low-friction.

- Segment denial reasons, choose the matching route (repair/secured/builder), confirm channel permissions, and ship a localized pre-lander with fees/timelines.

- Some exist, but approvals still depend on issuer rules; secured cards and builder loans are safer step-ups for many profiles.

- Intent content → compliant pre-lander (eligibility/fees/timelines) → repair or secured/builder path; confirm allowed traffic at the offer level and log weekly outcomes.