Affiliate marketing in financial services often looks attractive on paper: performance-based payouts, controllable acquisition costs, and scalable reach. In reality, many banks and fintech companies struggle to make it work. Approval rates fall below expectations, compliance teams raise concerns, and ROI becomes difficult to explain with confidence. The problem is rarely traffic volume. Most failures come from applying retail-style assumptions to a regulated, approval-based funnel.

This article explains how financial advertisers actually work with affiliate networks: how they use affiliate marketing as a channel, what they expect from CPA networks, why they choose networks over in-house setups, and how they design, launch, and scale compliant programs with predictable economics.

How banks and financial brands use affiliate marketing

Banks, lenders, insurers, and fintech companies use affiliate marketing as a performance acquisition channel, not as brand advertising. The goal is not impressions or clicks, but approved, funded, or activated customers that fit underwriting and risk criteria.

In practice, financial advertisers use affiliate marketing to:

-

acquire qualified applicants at a predictable cost

-

pay only for validated outcomes, such as approvals or funding

-

complement paid search and paid social with incremental reach

-

test new products, segments, or geographies with controlled risk

-

scale distribution without expanding internal sales teams

Affiliate marketing in finance is rarely a “top-of-funnel” channel. It sits closer to conversion, where intent is clear and economics can be measured against LTV, not just CPA.

What an affiliate network does in the finance vertical

In financial services, an affiliate network is not just a traffic marketplace. It acts as an operational and governance layer between advertisers and publishers.

Core roles

-

Advertiser: bank, fintech, lender, insurer, or brokerage

-

Publishers: comparison sites, content media, loyalty platforms, email partners, influencers, pay-per-call providers

-

Affiliate network: tracking infrastructure, contracts, payouts, compliance enforcement, fraud controls

Finance introduces complexity that generic affiliate setups rarely handle well. Claims are regulated. Conversions are approval-based. Funnels are longer. Partner vetting is stricter.

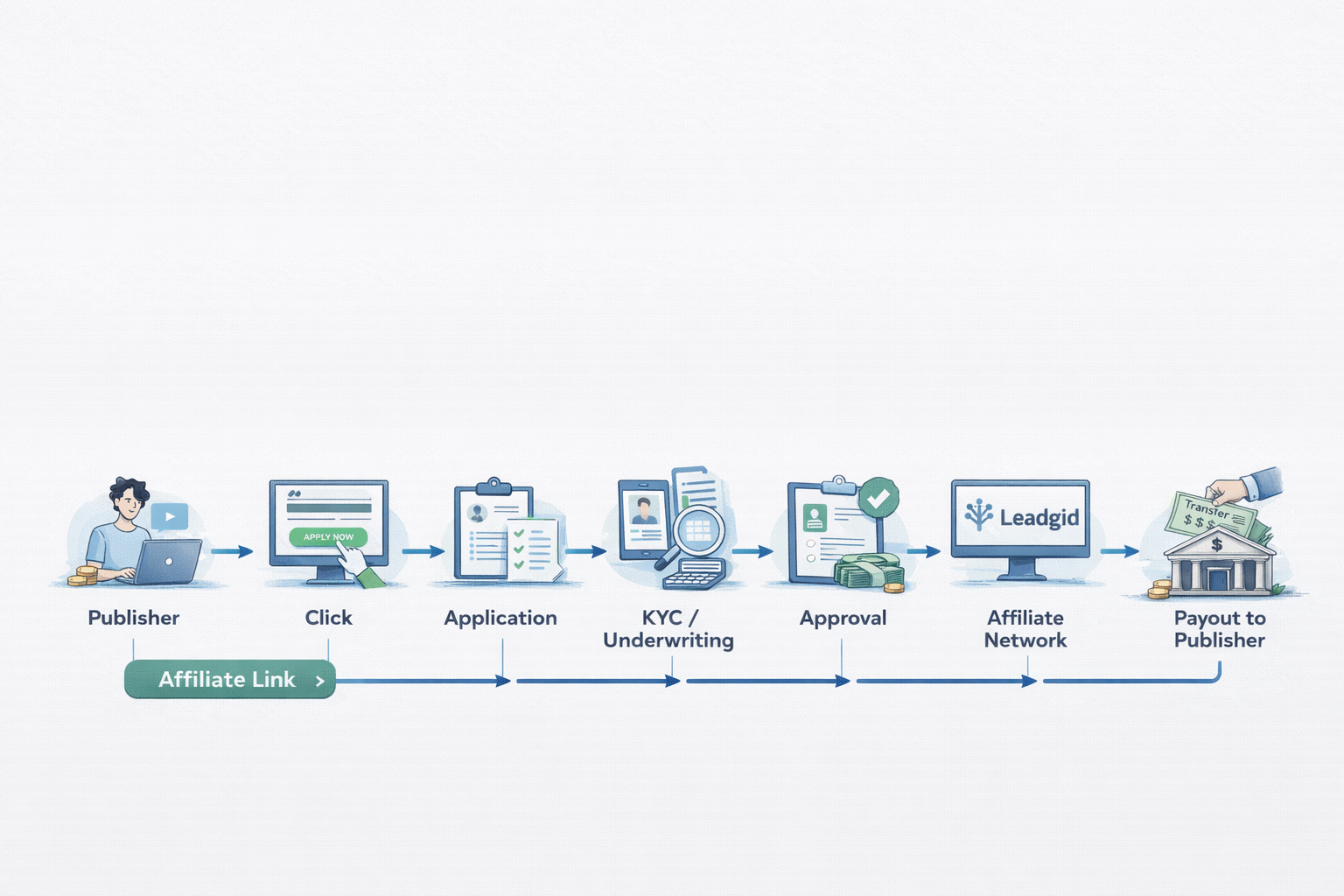

A typical finance affiliate flow looks like this:

What advertisers expect from CPA networks in finance

Expectations in finance are higher than in most affiliate verticals. Advertisers are not looking for “more traffic.” They are looking for control, transparency, and alignment with business value.

What financial advertisers expect from a CPA network

-

access to vetted, finance-capable publishers

-

tracking they can trust, including server-to-server postbacks

-

clear attribution and deduplication against other channels

-

enforcement of compliance and brand-safety rules

-

protection from fraud, duplicates, and low-quality volume

-

transparent reporting tied to approvals and funding

-

predictable clawbacks, reconciliation, and payment cycles

Networks that cannot provide these fundamentals tend to create volume without confidence.

Finance-focused networks such as Leadgid are often chosen by advertisers who prioritize approval transparency and partner governance over unmanaged scale.

Designing finance offers: conversions and commissions

Finance offers must be designed backward from value, not from traffic volume.

Defining the right conversion

Different products require different conversion points:

-

credit cards → approved application

-

banking → open + funded account

-

investing → funded account or first trade

-

insurance → policy bind

-

lending → approved or qualified application

Paying too early shifts risk to the advertiser and inflates invalid volume.

Commission models used in finance

|

Model |

Paid for |

When it’s used |

Main risk |

|

CPL |

Qualified lead |

Pre-qualification tests |

Lead quality |

|

CPA |

Approved / funded outcome |

Core finance programs |

Longer cash cycle |

|

CPS / RevShare |

Revenue over time |

Long-term value products |

Attribution |

|

Hybrid |

Mixed milestones |

Most finance offers |

Operational complexity |

A deeper explanation of payout logic, tiering, and risk alignment is covered in CPA, CPL, CPS in financial: payment models explained. Most mature finance programs rely on hybrid and tiered structures to balance scale and quality.

Regulatory and brand-safety controls

Compliance is not a separate step in finance affiliate marketing. It is embedded into the system.

Non-negotiables

-

no misleading or guaranteed claims

-

accurate APR, fee, and eligibility disclosures

-

clear affiliate disclosures

-

approved creatives and placements only

Operational enforcement

-

pre-launch reviews

-

automated monitoring and spot checks

-

documented escalation and takedown timelines

-

clawbacks and penalties when needed

A detailed breakdown of regulatory expectations, common violations, and risk scenarios is covered in Compliance, regulation, and risks in financial affiliate marketing. Most serious failures in finance affiliate programs are compliance-driven, not performance-driven.

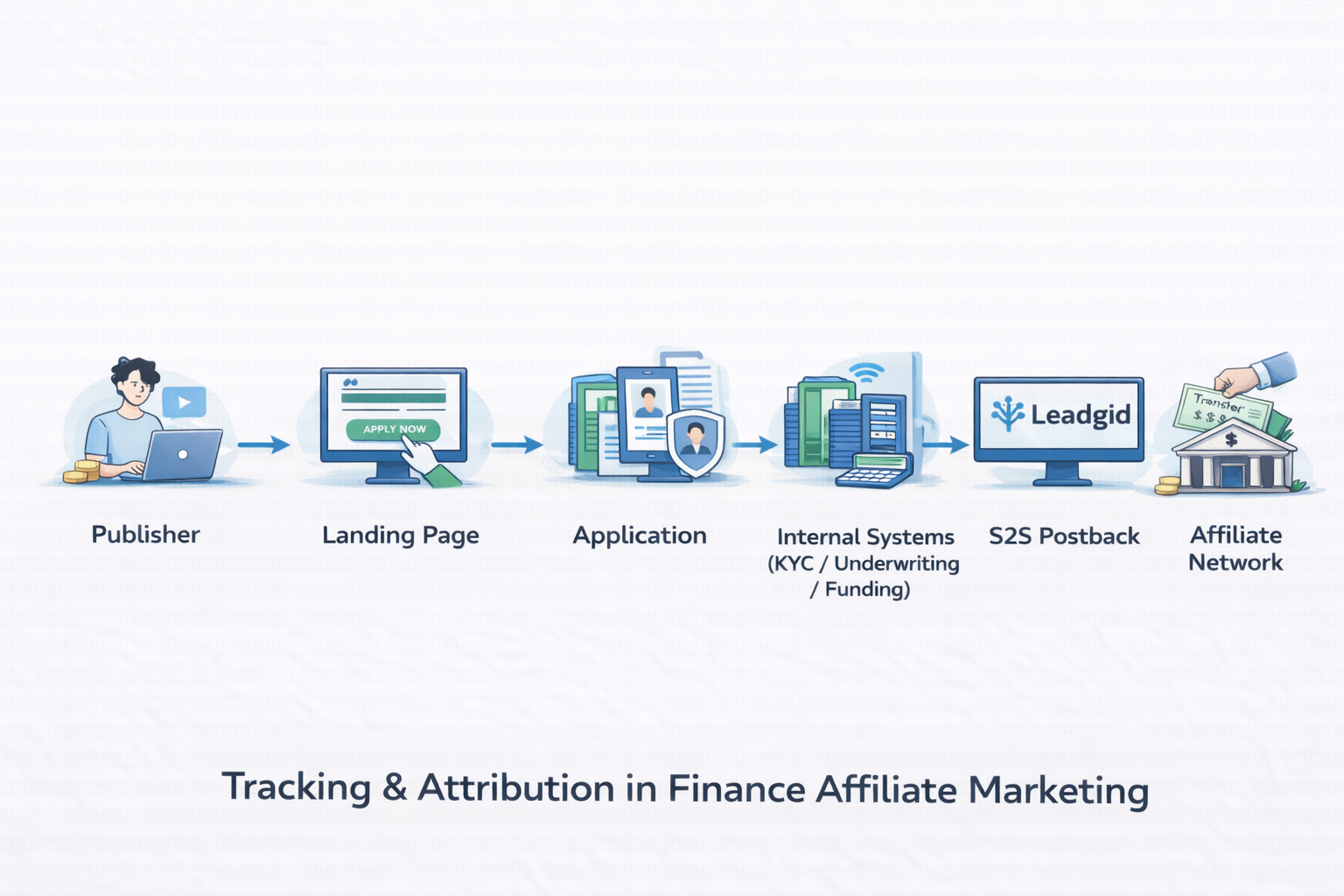

Tracking and attribution: getting data right

In finance, tracking defines truth.

Best practices

-

pixels only for upper-funnel signals

-

server-to-server postbacks for approvals, funding, and activation

-

persistent click IDs through the funnel

-

defined attribution windows per event

-

deduplication against other channels

-

offline approvals imported via CRM or call tracking

Without this, ROI reporting is unreliable.

Publisher types that perform well in finance

|

Publisher type |

What works |

Key controls |

|

Comparison sites |

Rate tables, filters |

Data accuracy |

|

Content / SEO |

Guides, reviews |

Claim libraries |

|

Cashback / loyalty |

Incentives |

Activation-based payouts |

|

Influencers |

Educational content |

Script approval |

|

Email partners |

Nurture flows |

Opt-in proof |

|

Pay-per-call |

High-intent users |

Call-length filters |

Clear briefs and approval workflows reduce risk and improve conversion quality.

Lead quality and fraud prevention

|

Risk |

Control |

|

Bots |

Device and velocity checks |

|

Duplicate leads |

Suppression lists |

|

Incent abuse |

Staged payouts |

|

Call spam |

Duration and routing filters |

|

Sub-affiliate abuse |

Transparency requirements |

Fraud prevention requires continuous monitoring and enforcement.

Metrics that actually matter

|

Metric |

What it shows |

Why it matters |

|

Approval rate |

Lead quality |

Core efficiency |

|

Funded / bind rate |

Real value |

Revenue alignment |

|

Activation time |

Funnel friction |

Optimization |

|

LTV : CAC |

Unit economics |

Scalability |

|

Clawback rate |

Risk |

Program health |

Financial advertisers use affiliate networks not for shortcuts, but for structure. Banks and fintechs choose affiliate marketing when they need measurable, approval-based growth with controlled risk. They choose affiliate networks because networks provide infrastructure, compliance enforcement, and partner governance that is difficult to replicate internally. When programs are designed around real outcomes, affiliate marketing becomes a predictable and scalable channel—even in highly regulated financial verticals.