If you wonder 'Can I use SEO for payday loan traffic?', then yes-if the specific offer allows SEO. Always check the Allowed traffic field and run a compliant flow: intent page → pre-lander (eligibility, fees, timelines, disclosures) → offer. Use permissioned lists, platform-safe wording, and keep evidence of consent, policies, and approvals.

Key takeaways

- Offer-level rules: Policies vary by offer and GEO; treat “Allowed traffic” as the source of truth.

- Pre-lander → approvals: Clear eligibility and cost/timeline notes reduce denials and complaints.

- Use your real channel: Prefer loan CPA offers that allow SEO/Email traffic (don’t force a disallowed source).

- Compliance is copy + process: No promise language, keep consent logs, save policy PDFs/screens.

- Iterate with evidence: Track Impr → CTR → Pre-lander CR → Submit → Approval → EPC and review “denial reasons” weekly.

What “Allowed traffic” means (and why it’s offer-specific)

Starting at fundamentals, “Allowed traffic” sets which sources you can use and under what conditions.

Typical statuses

- Allowed: Source is permitted as described.

- Restricted: Conditions apply (e.g., pre-lander required, GEO-limited SEO, email only for existing subscribers, social copy templates).

- Disallowed: Source not permitted.

Common conditions

- Pre-lander required (with eligibility bullets + disclosures).

- No trademark/brand bidding unless you have explicit written approval.

- Content requirements (e.g., rate/fee phrasing, disclaimers, T&Cs links).

- Channel-specific constraints (e.g., no lookalikes for certain audiences).

Run compliant loan flows on Leadgid - Sign up.

SEO for loan offers - safe playbook

- Target informational/intent queries (“how short-term loans work in [GEO]”, “installment vs payday”).

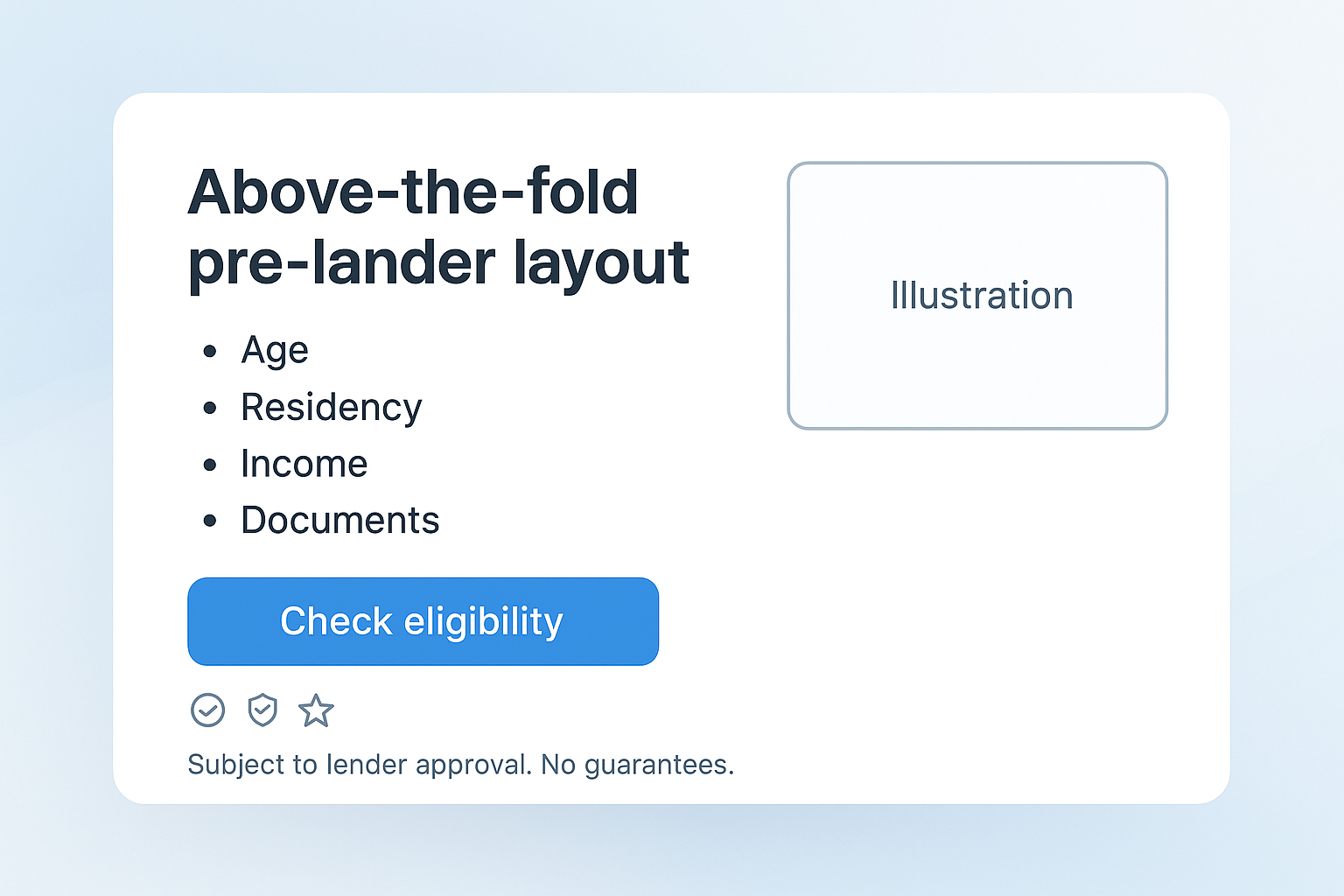

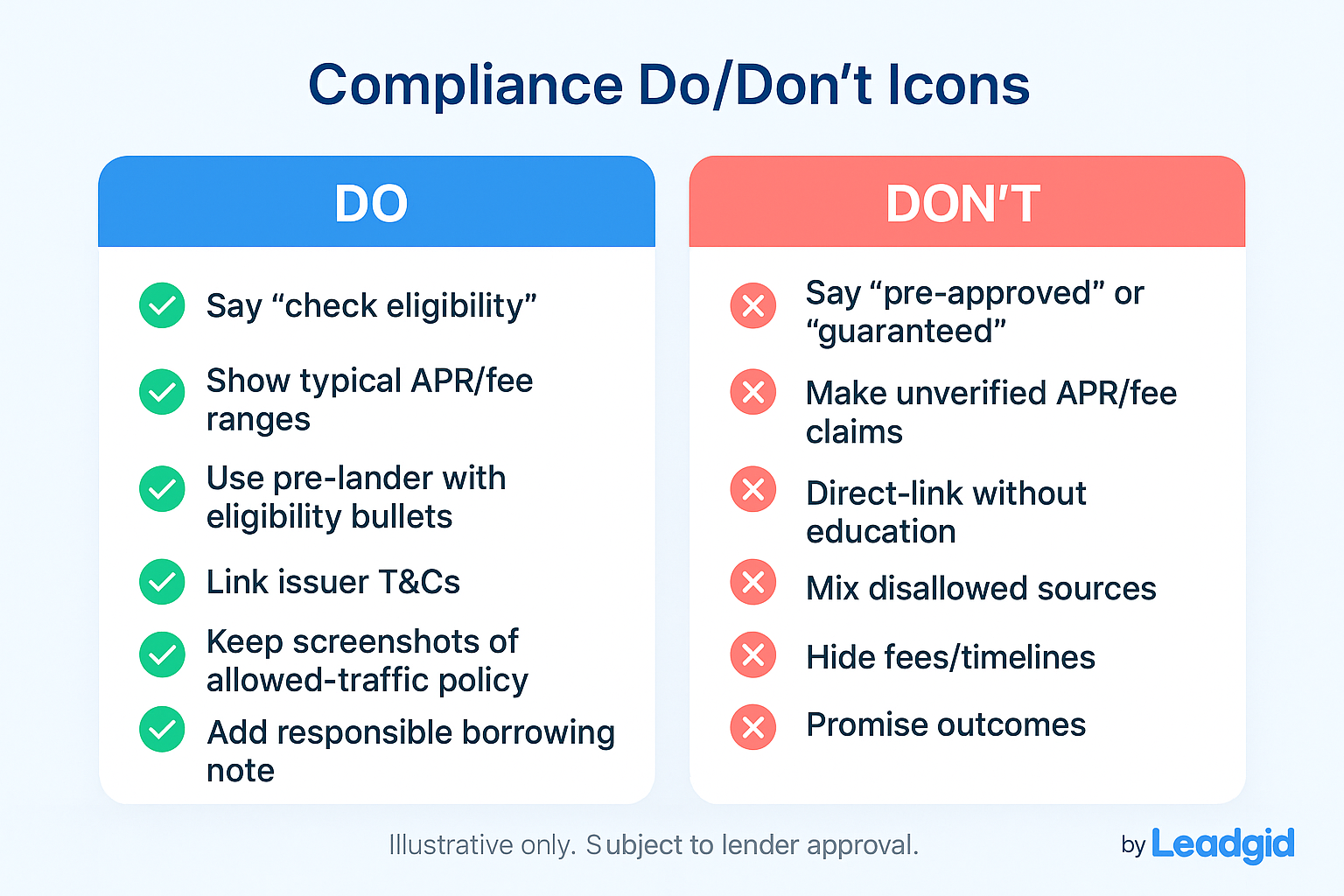

Common question: do I need a pre-lander for loan offers? - usually yes. Use it to pre-qualify:

- Eligibility bullets: age, residency, income, employment.

- Costs & timelines: plain-language fees, repayment cadence, late-fee risks.

- Disclosures: “subject to lender approval,” links to lender T&Cs, responsible-borrowing note.

- Technical hygiene: fast mobile pages, clear CTAs, structured data (FAQPage) for extractable answers.

Common question: brand bidding and loan affiliate offers, allowed or not? Typically no. Use generic/intent keywords unless the offer explicitly approves brand terms in writing. Explore deep dives into SEO and payout terms as well.

In SEO any detail matters. For example, a PH SEO test saw approvals improve when disclaimers were above the CTA.

Email - permissioned only (compliance basics)

- Email compliance for finance affiliates, tips on using:

- Use opt-in lists (record timestamp/source/IP); no scraped/bought lists.

- Clear sender, physical address (where required), and 1-click unsubscribe.

- Avoid deceptive subjects and promise language; be specific and educational.

- Flow: short education sequence → pre-lander → offer.

- Suppress non-engagers; document consent and suppression events.

Social / UGC - wording & disclosure basics and Facebook policy for loan ads 2025

- Use short, educational posts/videos; link-in-bio → pre-lander.

- Add disclosures (affiliate) where required; keep overlays/captions compliant.

- Platform rules change; keep a living doc of examples your manager approved.

Tips on Facebook policy:

- Always verify on the official policy page before launch

- Avoid guarantee language

- Target responsibly

- Expect extra review in finance.

Pre-lander & disclosure checklist

Must-have elements

✅ Eligibility bullets (age/residency/income/employment).

✅ Fees & timelines explained in plain language.

✅ “Subject to lender approval” disclaimer; no “guaranteed/instant approval”.

✅ Links to lender T&Cs and your privacy/consent notes.

✅ Responsible-borrowing reminder (budget impact, late-fee risk).

✅ Contact/support info and local service hours (where relevant).

Have us review your pre-lander - Talk to a manager.

Evidence & QA - stay audit-ready

- Save screenshots/PDFs of the offer’s Allowed traffic and copy rules.

- Maintain a change log (date, what changed, who approved).

- Keep consent evidence (email): timestamp, source, IP.

- Capture approval reasons weekly → update eligibility copy/targeting.

- Use UTMs + postbacks/API for cohort checks (source/geo/device).

Mini “How-to” - launch in 5 steps

- Pick one GEO & one offer; confirm allowed traffic for loan CPA offers 2025 in writing (and save it).

- Build the pre-lander; add eligibility, costs/timelines, disclosures; run it past your manager.

- Launch one permitted channel and one angle; no brand/trademark bidding without explicit approval.

- Measure: Impr → CTR → Pre-lander CR → Submit → Approval → EPC; fix the weakest link first.

- Weekly review with your manager; change one lever at a time (copy, targeting, device UX, offer). If policy blocks your channel, pick and switch offers, not rules.

And remember: Before any launch, confirm Allowed traffic in your offer and send your pre-lander for manager review.

Policy matrix - confirm before launch

|

Item to confirm |

SEO |

|

Social/UGC |

Notes |

|

Allowed / Restricted / Disallowed |

☐ |

☐ |

☐ |

Offer- and GEO-specific |

|

Pre-lander required |

☐ |

☐ |

☐ |

Use approved template if provided |

|

Brand bidding allowed? |

☐ |

- |

☐ |

Usually no; need explicit written approval |

|

Sample compliant wording |

☐ |

☐ |

☐ |

Keep a copy-bank; manager-approved examples |

|

Disallowed claims list |

☐ |

☐ |

☐ |

“Guaranteed”, “Instant”, “No checks ever” |

|

Sensitive audience rules |

☐ |

☐ |

☐ |

Platform & GEO variations apply |

|

Tracking & disclosures |

☐ |

☐ |

☐ |

UTMs, consent logs, T&Cs, privacy links |

Tip: Print this matrix for each offer. Don’t go live until every box is answered and stored.

Common mistakes (and quick fixes)

- No written policy.

Fix: request & save Allowed traffic confirmation and any channel caveats.

- Direct-linking without education.

Fix: add a pre-lander with eligibility + disclosures.

- Promise language.

Fix: replace with eligibility/estimate phrasing; add “subject to lender approval”.

- Brand bidding by default.

Fix: avoid unless explicitly approved; use generic/intent keywords.

- Unpermissioned email.

Fix: permissioned lists only; document consent and suppression.

- Testing many variables.

Fix: one channel, one GEO, one angle for 7–14 days; then iterate.

Summary

SEO can be an effective traffic source for payday loan offers-but only if it’s explicitly allowed for the campaign you’re running. Always double-check the Allowed traffic field and follow a compliant funnel: intent page → pre-lander (eligibility, fees, timelines, disclosures) → offer. Use verified opt-ins, clear policies, and maintain evidence of user consent and compliance at every step.

Offer rules differ by GEO and advertiser, so treat each offer’s terms as the definitive guideline. A strong pre-lander with transparent eligibility details and repayment timelines not only improves approval rates but also minimizes user complaints. Always work with your real, approved channel-if SEO isn’t permitted, choose Email or Native placements that are.

Remember: compliance is not just copy-it’s documentation. Avoid misleading claims, keep consent logs, and store proof of your compliance materials. Review your funnel metrics regularly (Impressions → CTR → Pre-lander CR → Submit → Approval → EPC) and use data to refine your flow.

In short, the answer to “can I use SEO for payday loan traffic?” is yes-but only when you’re following the rules, documenting every step, and optimizing responsibly.

Ready to launch? Start with an offer that explicitly allows your channel; we’ll help verify policies and optimize.

FAQ

- Yes-if the specific offer permits SEO. Use an intent page → pre-lander → offer; avoid promise language and keep disclosures clear

- They exist but are offer-specific. Confirm permissions in writing and follow any pre-lander or copy requirements.

- It varies by offer/GEO. Check if SEO, email, or social is Allowed, Restricted (conditions), or Disallowed, and whether a pre-lander is required.

- Usually recommended or required. It increases approvals by setting expectations and filtering in-profile users.

- Generally no, unless explicitly approved in writing. Use generic/intent keywords instead.

- Always verify the current official policy before launch; finance ads face stricter review. Avoid guarantees, target responsibly, and add clear disclosures.